The Changing Venture Landscape

Both Sides of the Table

SEPTEMBER 10, 2021

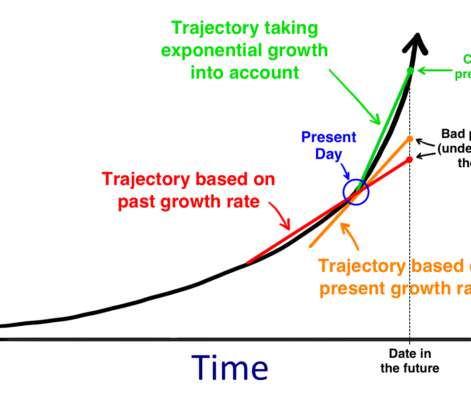

I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. On the one hand, you’re over paying for every investment and valuations aren’t rational. dot-com bonanza. Ten years on much has changed.

Let's personalize your content