What Does the Post Crash VC Market Look Like?

Both Sides of the Table

SEPTEMBER 15, 2022

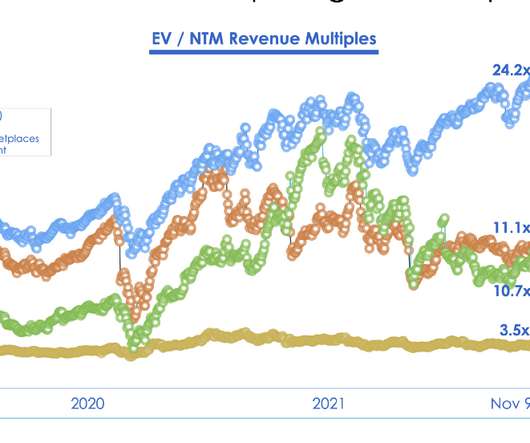

What You Can Learn From Public Markets It doesn’t really take a genius to realize that what happens in the public markets will filter back to the private markets because the ultimate exit of these companies is either an IPO or an acquisition (often by a public company whose valuation is fixed daily by the market). It’s just math.

Let's personalize your content