The Funding Cliff

There has been this recent obsession with this unfolding story of the Series A Crunch. Now we have data that shows “incontrovertible proof” that there is indeed a growing funding shortfall between seed stage startups and Series A startups. Well, after reading all of the reports and the data and the commentary, this is what I have concluded…so what.

For all the weeping and gnashing of teeth, the real story is that what we are experiencing is the natural ebb and flow of markets. In this case, the market is early stage investing. This blurb from the CB Insights report sums it up well:

Despite the concerns about a crunch, the reality is that the level of Series A activity is holding steady. At the same time, the number of seed deals have exploded. As a result, the Series A Crunch is nothing more than excessive demand for a limited supply of Series A financings.

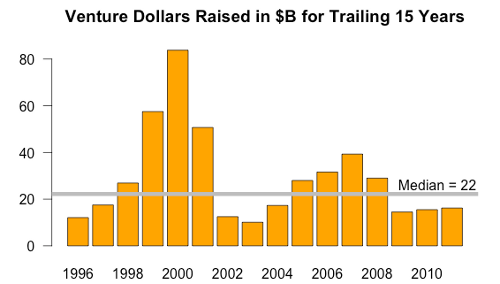

The amount of money raised by venture capital firms has not grown appreciably over the past several years, and what is raised is being concentrated in fewer and fewer firms.

The result is that there is not all that much more money available for entrepreneurs than there was before the recent financial crash. This is in spite of all the mega rounds that many top funds have announced.

At the same time, more and more money is being poured into seed funding. This is fueled in part by the publicity generated by the media about high flying startups which has drawn more would be entrepreneurs and investors into the mix. Investors feeling left out of the gold rush started placing small bets as options in early stage startups to get ahead of “next big thing”. Then many non-traditional investors got involved, to the point where it seems like a new seed fund or accelerator is launching every few days.

However, you get these strange articles that sound all doom and gloom or take an “I told you so” slant. The one billion dollars that will potentially be lost because of the Series A crunch sounds like a big of a number until it is stacked up to the hundreds of billions pissed away on bad post-Series A deals during the past decade. Markets eventually equalize, so I suspect that more money and more funds will fill some of the gap at the Series A level. But more importantly, what we are seeing is the new normal and that gap will continue to exist because more and more people are forming startups and there is a growing pool of early stage funding available from a growing number of sources and channels like crowdfunding portals and corporate-based startup initiatives.

If anything, this dreaded cliff should result in some positive effects. It is creating a virtuous cycle where talent is created and recycled throughout the tech startup ecosystem to successful startups starved for talent. In general, we are seeing more talent pouring in and more creativity spurred on and more innovative ideas generated by the community. The vast increase in startups means more ideas can be tested leading to even more innovative approaches and ideas. All of this is happening more cheaply and faster than ever before, creating opportunities for startups that is not as binary as success or fail, but rather a range of positive outcomes. In other words, we are in the nascent era of the innovator’s age.

There are only two questions that really matter for the entrepreneur; does this make the tech ecosystem inherently unstable (i.e. is this a bubble) and does this affect my ability to raise the next round? The answer to the first question is no, but the answer to the second is something to consider. You are competing with more startups for a pot of money that has not grown appreciably in a pool with fewer investors. I want to emphasize that last point, even if there was more money available for VC’s to invest, there is no extra capacity available for VC’s to evaluate and execute more deals. Therefore, until the market self-corrects, the main constraint in fund raising will be time and that will make the road difficult for the current crop of seed funded startups.

Given this situation, there are two key points to take away from the findings. One, make sure you have enough funds from your seed round to last. It takes over 13 months according to the data to raise the next round, but that is an average at best. You really need to make sure you have funds to last you for a solid 18 months. Two, take seed funding from investors that will be good partners including VC firms. While signaling could be an issue, it apparently has not hurt as many startups as previously thought. In other words, if the money is offered, it might be best to take it in order to give yourself the best chance to jump the seed/Series A chasm later.

6 Notes/ Hide

ingersollnik liked this

ardsfogo-blog liked this

stepwise-blog liked this

marksbirch posted this