How to Fill Your VC Fundraising Pipeline

Everyone starts their fundraising the same way:

1) Open a shared Google Sheet.

2) List all the VCs you've ever heard of.

3) Ask a bunch of people who they know.

4) Find out very quickly this isn't very effective.

First off, most people in the world can't name any VCs. I suppose if you're reading this post, you can name at least one--but I'm not even active anymore, so even if you could name a few, you might quickly find you have a relevancy problem.

Does this VC that you know do this kind of deal?

Do they do deals at your stage?

Is the firm still active?

Starting from a blank Google sheet and getting to the point where you have 20, 30, 50 or more *qualified* leads of investors for whom what you're doing is a fit is a very tall order.

Unfortunately, most of the databases out there dont quite make it easy for you to just say, "I'm X, who is looking for me?" and get an autogenerated list.

And yes, I tried ChatGPT. ChatGPT's data is two years old and when actual tech humans can't really differentiate easily between pre-seed and seed, who's a lead and who isn't, and whether or not someone is a real fund or just a broker, I wouldn't expect a bot to.

The problem is that the nomenclature very poorly describes what someone is actually willing to look at in any given moment. When you're applying to pre-schools, programs give clear cutoff dates. If your child was born before X date, you're either eligible or too late.

VC doesn't have those clear cutoffs.

Am I still pre-seed? I have revenue.

Do I pitch a consumer tech investor for my website that sells custom-fitted undershirts? Or is that only specifically people who say "D2C?'

Do you generally do pre-product or only when it’s your former analyst?

Plus, searching for what someone did in the past doesn’t necessarily guarantee they’re going to be interested in the future.

So how do you actually create a list that not only has enough names but has high-quality, relevant leads that will at least turn into meetings?

One word: Manually.

Step One: Top of Funnel

How do you actually build the list??

There are three main sources:

1) Other founders who raised *recently* in related areas. Even if you don’t know other founders well, founders are usually up for helping other founders. So, if you talk to folks who have raised a similarly sized round for something that isn’t competitive, but at least it’s in the same kind of ballpark, you’ll probably have some success asking if they’d be willing to share their lists.

You could also accomplish this by poking around on Twitter for posts where people have asked “Who are the top B2B SaaS pre-seed founds?” and a bunch of people have already responded. Still, don’t substitute that for live conversations.

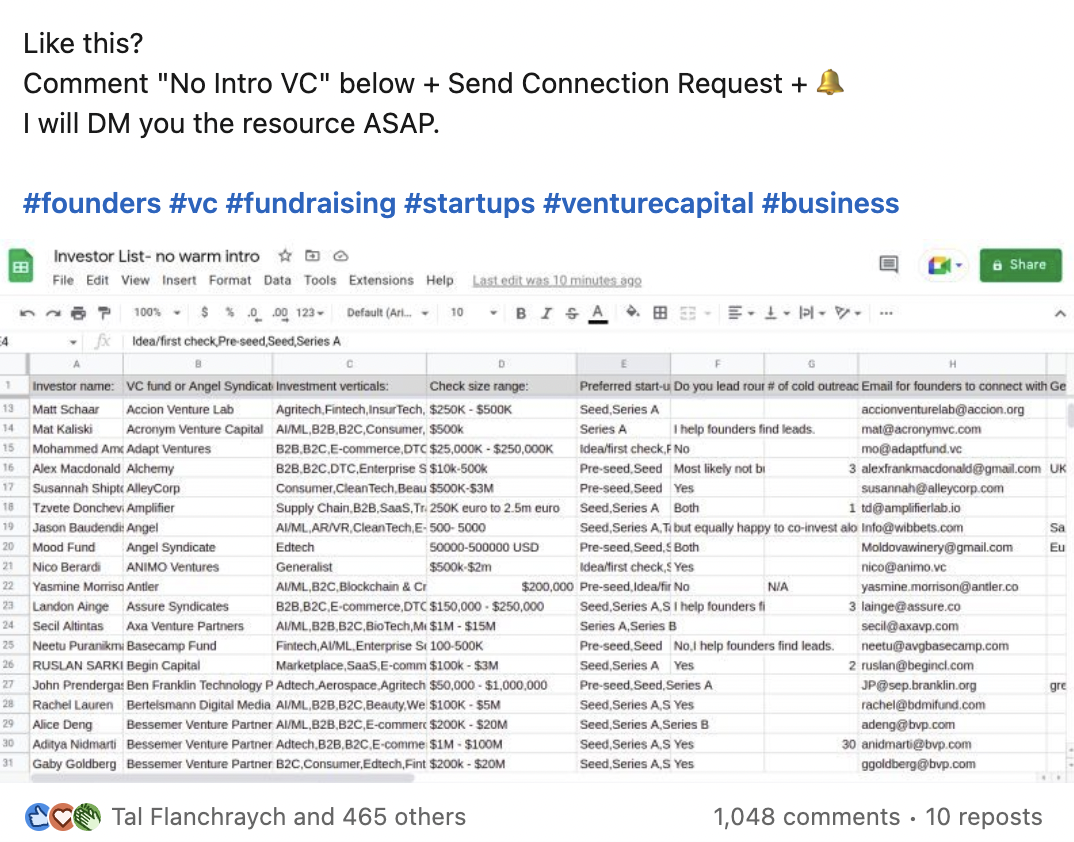

2) Big lists other people are using for clickbait. Search LinkedIn posts for “VC lists” and you’ll get a lot of public postings like this one:

There’s also Shai’s list of sub $200mm funds, this VCSheet database, this list of VC lists, OpenVC, etc, etc. Between all of these, you should have a pretty decent starting place.

3) Reverse engineering Crunchbase. Grab a free trial and start sourcing names by doing searches of similarly staged companies in the same basic verticals that have recently raised. You’ll wind up with a list of rounds and you’ll have to go through all the investors for those rounds, which can be very time consuming, but it will give you a good sense of who is still active.

Step Two: Qualify

So what do you then do with this spaghetti-on-the-wall list of funds? That’s when you have to do lots of manual work to click through each fund to confirm stage and sector via their websites—and to specifically pick out partners who would be the right person to pitch to.

A quicker way to do this might be to float this list by other people who have raised, friendly VCs at different stages or junior professionals at firms that have perhaps passed, but who still want to be helpful.

Someone in the know can sort out a list of 100 firms just by telling you verbally yes/no/yes/yes/no/too late/too early/no longer active as you tick down each row than you could ever do manually.

The process of qualifying these lists to make sure the firms are relevant is, unfortunately, a line-by-line process—one that involves lots of phone calls, e-mails, poking around, and lastly—and most importantly, asking the investors to qualify themselves.

That’s right—sometimes, in order to save yourself a lot of time, you need to just come out and say:

“My name is George. I'm unemployed, and I live with my parents.”

Or, at least, the startup equivalent of that.

That iconic line is so instructive in how it forces the respondent to one side of the fence or the other. George isn’t pretending to be something he’s not. He’s putting it all out there—knowing that most women would probably say no, but should he get a yes, he’s got a decent chance of success from there.

For a startup, that might be something like, “I’m a formally incarcerated founder who has been developing a six-figure personal training practice over the last 10 years. Through this career, I’ve discovered an opportunity to build a new type of connected barbell that could increase the average trainer’s take-home salary by 50% while decreasing their hours worked by a third. We’re pre-product and looking to meet with lead/first check investors in our pre-seed round to get our proof of concept out into the wild.”

The thing about such a pitch would be that it would unlikely to generate time wasting/tire-kicking meetings. You’ve already thrown out the biggest reasons why someone might say no—the founder’s background, the stage of the company, and the fact that it’s hardware. Anyone still taking a meeting is essentially pre-qualifying themselves as a decent lead—as opposed to what you would get if you offered this:

“I’m a first-time founder looking for support and guidance for my new company. I built a six-figure personal training practice over the last 10 years and I’ve discovered an opportunity to increase the average trainer’s take-home salary by 50% while decreasing their hours worked by a third. We’ve got 5,000 trainers in our alpha group and there’s lots of excitement around the product.”

A lot of people might take meetings around this pitch only because they’re curious why 5,000 people are doing something—only to find out that you scraped 20,000 names from the National Association of Fitness Professionals member database and stuck them all on an e-mail newsletter, and the 5,000 people aren’t even sure what the product is yet but are too busy to unsubscribe.

Whatever you do, don’t be too precious about certain firms or connections.

If you’ve got it in your head that one partner is the ultimate partner for you or that one person in your network is going to provide all these leads and it just doesn’t seem to happening with them—don’t overspend time on what appears to be a perfect opportunity. Focus on where you’re actually getting traction and remember that it’s going to take a lot of outreach and calls (i.e. time) to get anywhere in a fundraising process—so you shouldn’t get stuck on one line in a lead list and waste too much time on it.