What Does the Post Crash VC Market Look Like?

Both Sides of the Table

SEPTEMBER 15, 2022

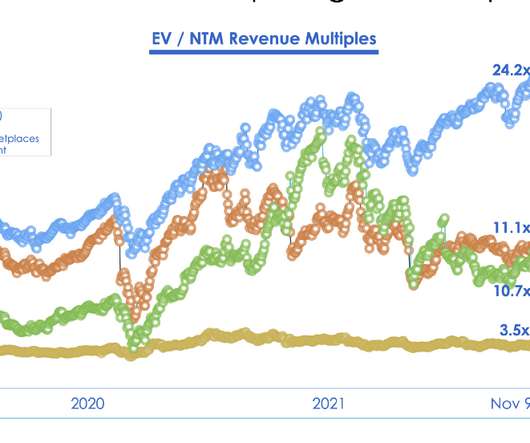

We drew this conclusion after a meeting we had with Morgan Stanley where they showed us historical 15 & 20 year valuation trends and we all discussed what we thought this meant. Should SaaS companies trade at a 24x Enterprise Value (EV) to Next Twelve Month (NTM) Revenue multiple as they did in November 2021? And reset they must.

Let's personalize your content