What Does the Post Crash VC Market Look Like?

Both Sides of the Table

SEPTEMBER 15, 2022

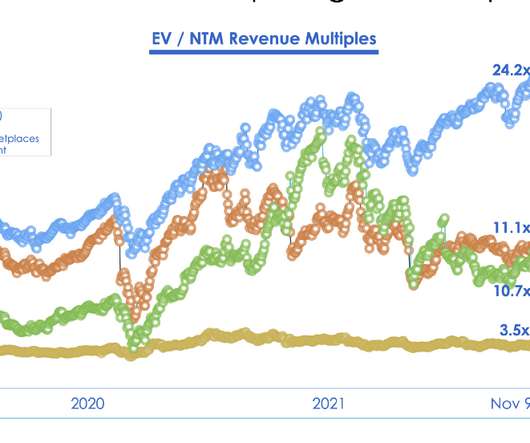

The market was down considerably with public valuations down 53–79% across the four sectors we were reviewing (it is since down even further). ==> Aside, we also have a NEW LA-based partner I’m thrilled to announce: Nick Kim. First in late-stage tech companies and then it will filter back to Growth and then A and ultimately Seed Rounds.

Let's personalize your content