How is the VC Asset Class Doing?

View from Seed

DECEMBER 4, 2019

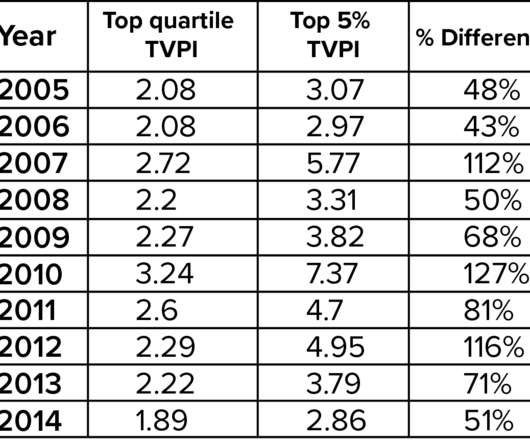

One of the things I pointed out in my prior post was that even though the 2007 vintage was 10 years old, the vast majority of the value was still unrealized. If we compare the 2007 vintage data today vs. what we looked at 2 years ago, it gives us a sense of how much liquidity that vintage has enjoyed in the last couple years.

Let's personalize your content